Protein is arguably the most mature category within the active nutrition industry, with decades of consumer familiarity and a well-established product hierarchy: concentrate sits below isolate, clear commands a premium, more filtration and refinement means a higher cost. So you’d think that pricing would be relatively straightforward. But once you start digging into the data, you quickly see that it isn’t.

Protein pricing: what the data tell us

At a macro level, yes, pricing is as you’d expect.

In Europe, median price per serve climbs steadily from whey protein concentrate (WPC) at €1.16 to whey protein isolate at €1.43, with blends and hybrids sitting in the middle and clear whey commanding a premium at €1.60.

The US and Canada mirror this, with WPC averaging $1.65 per serve and clear whey stretching to $2.56.

But within brand portfolios, this logic becomes less certain and products that you’d think might sit at a higher price point don’t always. Take native whey, for example. Across a range of brands, native whey is positioned as the more refined, premium option, and yet it’s often priced on par with, and occasionally below, standard equivalents.

If native whey is genuinely premium, why is that premium not consistently expressed in price?

One explanation is consumer engagement. While native whey may resonate with certain, more engaged audiences, it might just not be well enough known or understood to withstand aggressive pricing.

Protein price extremes

Things are even more pronounced at the extremes of the pricing scale. At one end, we have protein that’s entirely commoditised, retailing at a fraction of the median price per serve, while at the other end clear protein commands more than double the category median.

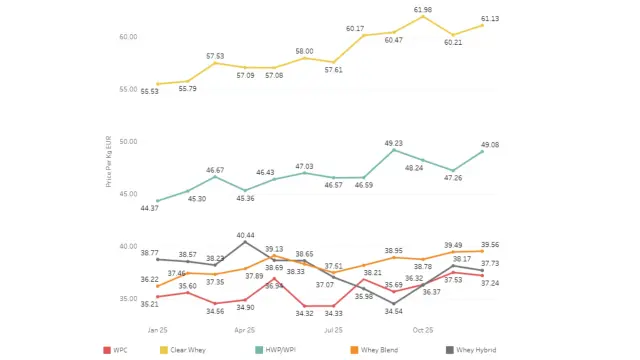

And inflation has only intensified this. Over the past twelve months, clear whey has seen a 10% increase in price per kilo across Europe to sit at €61.13 per kilo while whey protein isolate has climbed 10.6% to €49.08. This is well ahead of most other formats that typically come in between €34 and €40. Raw material pressure is clearly being passed on to consumers, particularly in premium, performance-led segments where brands believe willingness to pay remains strongest.

Interestingly, whey hybrid pricing has decreased slightly over the same period, suggesting brands are increasing the proportion of lower-cost protein sources within blends to manage costs.

Protein pricing as a strategic lever

Within the protein market, there is no single, universally accepted price anchor. While the mid-market may follow a typical, quality-based hierarchy, within portfolios and at the extremes, price is governed by narrative strength, audience targeting and strategic priority. Raw ingredients may set the baseline, but brand strategy determines the final number on pack. Through storytelling, trust and positioning, brands must then justify their worth.

Protein pricing may appear technical but in reality, it’s deeply strategic.

.jpg)

.jpg)

.jpg)

-min.jpg)

.jpg)